Taxation has long been based around the physical presence of a business in a particular country.

The huge expansion of the digital sector has, however, challenged our preconceptions. Many people would argue that if a global tech firm, for example, makes profits in a particular country, they should be taxed there – regardless of whether they have offices, plants or facilities in the jurisdiction.

Governments and global tax authorities are currently working together on a more uniform and coherent approach to the digital economy. And as part of this process, HMRC are proposing a significant change.

Right now, if a UK company pays royalties for the exploitation of intellectual property and similar rights to overseas entities, they are subject to the deduction of UK tax at 20%. The only exception is if there’s an international agreement to reduce this amount.

The UK now proposes to include payments made by a non-UK entity to a fellow non-UK connected party in a jurisdiction (often with low or zero tax), with which the UK does not hold a suitable double tax treaty.

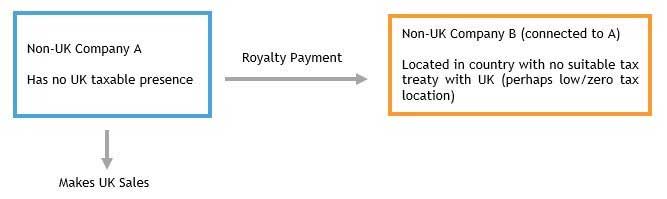

In the example below, Company A derives UK income, but has no UK taxable presence and pays no UK tax. It may obtain a tax deduction in its location of residence for the royalty it pays to B. If B is in a location which has low or zero tax, the structure is very efficient.

Under the proposed reform, a 20% UK tax could apply on the royalty paid from A to B. It closes a loophole, but may have a wider scope than imagined, as it signals a radical shift away from current principles on the taxation of cross-border payments.